Digital Card Solution

In today's fast-moving world, it's more important than ever to offer seamless banking services.

Deliver the digital-first payment experiences your cardholders expect. Entrust gives you the tools you need to issue secure, instantly available cards right from your banking app.

of people prefer to do their daily banking online.

Source: Digital-First Banking Report

of U.S. financial institutions say cybersecurity breaches are their most immediate fraud concern.

Source: U.S. Financial Trends Report

of people prefer digital credit and debit cards.

Benefits of the Entrust Digital Card Solution

Instant Card Issuance

Securely issue digital cards in seconds in your banking app — with no need to wait for the mail.

Higher Card Activation & Usage

Over 95% of cardholders use their digital card on day one. Push provisioning to Apple and Google Pay ensures top-of-wallet placement.

Lower Fraud Risk

Digital-first transactions reduce fraud by 20–25% on average, thanks to tokenization, biometrics, and chip-grade authentication.

Reduced Servicing Costs

Give customers self-service access to PINs, token controls, and card credentials, cutting support costs by up to 40%.

Simple, Scalable Deployment

Use one SDK to enable all digital card use cases — including Push to wallets, Click to Pay enrollment, NFC Issuer wallet, and token management — with zero back-end integration required.

Increase Customer Acquisition

Digital card issuance drives a 10–15% average increase in new customer acquisition by delivering instant access to spend-ready accounts.

Enable Digital Wallet Enrollment From Any Web Browser and Device

Make digital wallet enrollment accessible, simple, and secure — even without a mobile app. Entrust Digital Card Solution Web Push Provisioning enables cardholders to add their payment cards to Apple Pay or Google Wallet from any browser on desktop, tablet, or mobile. Eliminate manual card entry, accelerate activation and time to first spend, and support modern digital wallet requirements across all card programs.

Seamless, Secure Checkout Experiences

Make online checkout safer, faster, and simpler. With Entrust, banks and credit unions can easily allow cardholders to enroll into Click to Pay — a tokenized EMVCo solution — from within their mobile apps. Cardholders enjoy one-click payments across major retailers like Visa and Mastercard, while you reduce fraud and meet global compliance standards.

Enable Tap-and-Pay in Your Banking App

Deliver a seamless tap-and-pay experience directly within your banking app — on both Android and iOS. Entrust’s NFC Issuer Wallet empowers financial institutions to create their own, fully branded, secure, and seamless digital payment solutions. With a single SDK integration, financial institutions can digitize cards, own the CX, and boost app engagement.

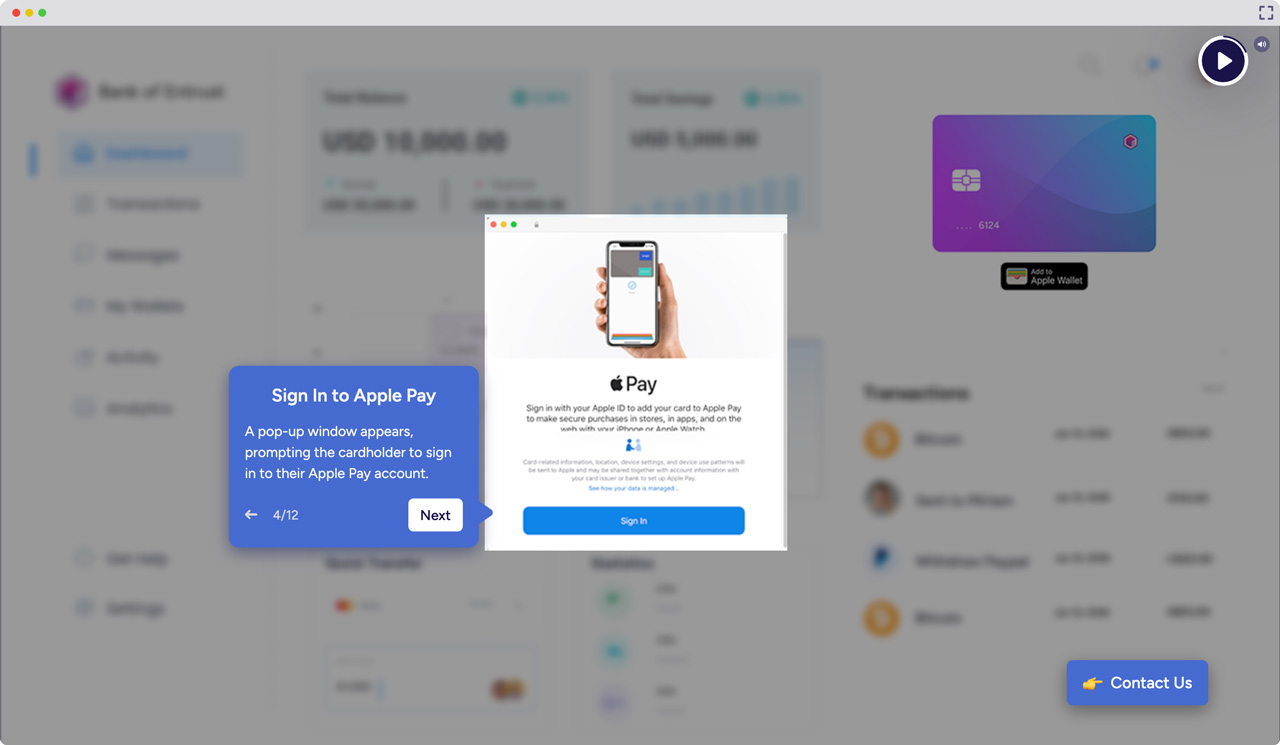

Enable Web Push Provisioning for Broader Reach and Faster Card Activation

Entrust Digital Card Solution gives your cardholders more ways to add cards to digital wallets with web push provisioning. Explore our demo to see how easy it is to add a card to Apple Pay from any web browser.

Modernize the Cardholder Experience

Push Provisioning to X-Pays

Add cards to Apple Pay, Google Pay, and Click to Pay using a mobile app or web interface—secure and seamless.

Secure Card Display

Show full card details in-app that allow users to view, copy, or autofill card details securely – PCI-DSS compliant.

NFC Issuer Wallet

Enable tap-and-pay directly from your banking app on iOS and Android — no third-party wallet required, with full issuer branding and control.

Token Manager

Let users manage their own card tokens — view wallet activations, suspend devices, or remove cards — all from the banking app.

Pay by Account

Let users pay directly from their bank account — no card required — using tokenized account credentials for in-store and online Mastercard payments.

PIN Display & Change

Enable in-app PIN view and self-service PIN changes — enhancing security while reducing help desk calls.

Click to Pay

Offer seamless enrollment into Click to Pay, from within your banking app, compliant with scheme requirements.

Issuer Token Service Provider (iTSP)

Accelerate time to market and enable seamless wallet integration across OEM Pay, wearables, and e-commerce. Entrust’s Issuer TSP Hub helps simplify digital card issuance and token lifecycle management through a single, secure connection.

Strong Customer Authentication

Meet global regulations and protect transactions with chip-grade security, biometric login, and adaptive MFA.

Go Digital-First with Entrust

Deliver digital cards instantly and securely — right from your app. Learn how Entrust helps banks create fast, seamless payment experiences.

Proven in the Marketplace

Trusted and vetted by the world’s leading payment ecosystem providers.

Mastercard Engage Excellence Awards 2024 & 2025:

1st place for innovation in the "Issuance" category

Entrust is a Certified Visa Ready Partner

Entrust Customers Share Their Success Stories

![]()

Adrien Fournier, Marketing Director, Noelse

The implementation of the solution was very seamless thanks to the technical expertise of the Entrust Digital Card Solution teams.

![]()

Marko Rankovic, Executive Director & General Manager, Raiffeisen Processing Center

Entrust is a valuable partner of RPC in bringing continuous innovation and added value to our customers. We are confident that RaiPay will continue to grow and play a significant role in helping clients to pay securely and conveniently.

![]()

Bilal Faiz Al Raisi, AGM and Head of Cards and Bancassurance at BankDhofar

We were one of the first banks in Oman to launch Tap to Pay services and will continue to lead in that direction with tokenization services

![]()

Mohammed FIKRAT, President of Crédit Agricole du Maroc

We wanted to tap into the Entrust Digital Card Solution to become one of the first banks to launch these digital capabilities and position ourselves as one of the leaders in banking and payments innovation in Morocco.

![]()

Maher Mikati, CEO of areeba

Entrust’s ability, responsiveness, and shared vision for innovation were instrumental in helping us achieve this major step, which aligns with areeba’s vision to broaden access to digital financial services and support Lebanon's evolution into a cashless economy.

![]()

Deepak Baran, Head of Financial at Vodafone Fiji

With these advancements, Vodafone Fiji continues to lead in delivering instant, secure, and convenient financial solutions to its customers.

![]()

Laks Vasudevan, Retail Payments Director at Huntington Bank

Our collaboration with Entrust will further strengthen our enhanced digital wallet capabilities, adding valuable payment features for our customers.

![]()

Daumantas Barauskas, Genome’s Chief Executive Officer

Leveraging the Entrust Digital Card Solution gives our cardholders the ability to place their digital card in any third-party e-wallet so they can pay in the way that’s most convenient for them. We are excited about this partnership.

![]()

Mr. Johnny Torbey, CEO, IPN

Entrust gave us the flexibility and expertise we needed to launch Google Pay in Lebanon – without compromising on neutrality or scalability.

![]()

Danny Robinson, Credit Bank PNG's Chief Executive Officer

With Entrust, our customers can now open an account entirely online and instantly receive a virtual Visa card – no branch visit required.

![]()

Nikola Dzambazovski, Ph.D., Chief Sales and Development Officer and Board Member, Komercijalna Banka AD Skopje

Leveraging the Entrust Digital Card Solution Issuer TSP hub and SDK was the right decision to accelerate the launch of Google Pay and to enable seamless card digitization into Google Wallet for our cardholders.

Related Resources

U.S. Financial Trends

See how decision makers are shaping the future of U.S. card issuance, focused on the opportunities and strategies for financial institutions.

Payment Modernization Tips

Backbase CMO welcomes Tony Ball of Entrust for an in-depth conversation on how banks can re-architect their operations to stay ahead and deliver a breakthrough customer experience in a rapidly evolving landscape.

An IT Team’s Guide to Enhancing Your Bank’s Digital Card Strategy

Find out how banking IT teams can take digital card programs to the next level.

Seamless Digital Card Issuance

Learn how one software development kit can deliver a seamless digital card experience.

Huntington Bank Selects Entrust To Enable Digital Wallet Capabilities

See how the Entrust Digital Card Solution enables frictionless provisioning from mobile apps to third-party digital wallets.

CreditBank PNG Partners With Entrust to Deliver Digital-First Banking Experience in Papua New Guinea

See how the Entrust Digital Card Solution enhances digital banking in Papua New Guinea.

Digital-First Banking Report

Discover consumer banking preferences, plus the opportunities and challenges for digital banking in financial institutions.

Quick Pulse Survey

Find out what today’s banking customers are looking for and how to provide it.

Pay by Account

Discover how Entrust’s Digital Card Solution empowers financial institutions to enable Pay by Account payments seamlessly.

See how Entrust and Mastercard are making it easy to onboard new customers securely.

Entrust Enables European Issuers to Create Their Own NFC Issuer Wallet on iOS Devices

Learn how Entrust helps European issuers transform their banking apps into fully branded digital wallets.

Web Push Provisioning

Learn how banks, credit unions, and other card programs can enable secure, browser‑based digital wallet enrollment – including for issuers without a mobile app.

Fill out the form to have one of our experts contact you to discuss how you can create digital-first payment experiences for your cardholders.